Contents

- What does offshore mean? What is an offshore company?

- Offshore company pros and cons

- How to choose the right jurisdiction for incorporation of a company?

- What is the procedure for incorporating an offshore company?

- Stage 1 – it is necessary to decide on important corporate aspects

- Stage 2 – it is necessary to provide documents for the directors, shareholders, beneficial owners, and attorneys

- Stage 3 – it is necessary to undergo a compliance check

- Stage 4 – it is necessary to pay for company incorporation and accompanying services

- Stage 5 – it is necessary to prepare a package of documents for company incorporation

- Stage 6 – it is necessary to apply for company incorporation

- Stage 7 – it is necessary to complete company incorporation

- What is the incorporation time for an offshore company?

- Can the company’s jurisdiction be changed after incorporation?

- Can the name of an already incorporated company be changed?

- What does the subsequent maintenance of an offshore company include?

- Can an account be opened for an offshore company?

- Is automatic exchange of information relevant to offshore companies?

What does offshore mean? What is an offshore company?

Offshore jurisdictions are jurisdictions that offer non-residents special conditions for doing business; companies using such special conditions are called offshore companies. As a rule, for a company to be considered an offshore one, its owner (the beneficial owner) must reside outside the jurisdiction where the company is registered, and the company itself does not have the right to do business in the country of incorporation. Complying with these two basic conditions allows these companies to be exempted from tax in their country of incorporation. But offshore companies are required to annually pay a certain government fee.

Tax exemption in the country of incorporation does not mean that such companies need not pay tax at all! Offshore companies are required to pay taxes prescribed by the laws of:

• the countries in the territory of which they operate; and/or

• the countries in which their beneficial owners are tax resident.

Offshore companies are usually prohibited from conducting licensable business activities (for example, banking, insurance, etc.). Such activities are generally only permitted to local resident companies. This is because these activities require greater control by the state. Accordingly, the state wants to receive tax revenues from companies engaged in such activities.

But the situation in the offshore sector is gradually changing … Due to the global trends:

• to step up the fight against tax evasion (which includes eliminating “double non-taxation” of companies from offshore jurisdictions, when a company does not pay tax either where it is incorporated or where it does business),

• to step up the fight against money laundering and terrorist financing, and

• to increase transparency and openness in general in everything related to the operations of offshore companies, many classic offshore jurisdictions are making changes to their regulations for offshore companies.

So what are these changes?

Some jurisdictions are introducing the requirement for (economic) substance in the country of incorporation. This requirement does not apply to all offshore companies, but only to those that conduct “relevant activity” (the list of activities that qualify as relevant will vary in each such jurisdiction). Such companies must become tax residents in the country where they are incorporated and show their adequate presence there (the adequacy of the presence is determined individually in each specific case and depends on many factors).

Interestingly enough, the “relevant activity” usually includes, among other things, banking and insurance businesses which, as we already know, have traditionally been inaccessible to offshore companies. Consequently, we see offshore companies in a way becoming on par with local resident companies.

Companies that do not conduct the “relevant activity” carry on as usual, but need to file additional forms to government authorities to confirm that they do not conduct such activity. In this case, we are witnessing the manifestation of a global trend for greater transparency.

Other jurisdictions are moving towards equalization of offshore and local companies in terms of their rights and status: offshore companies are allowed to operate in the country of incorporation, deal with residents of the country of incorporation, and own real estate in the country of incorporation, all of which was previously prohibited. At the same time, territorial taxation is being introduced, which means tax only applies to income received by such companies from sources in that particular jurisdiction. Effectively, if a company continues to comply with all the restrictions that existed before, it retains its “offshore status” and even gets new opportunities. One thing to note though: there is an additional obligation to file certain forms with government authorities. One can say that transparency of business operations of offshore companies increases, but at the same time, they are still exempt from tax in their country of incorporation if they do not do business there.

You can also see the simultaneous application of the two mentioned approaches: the introduction of both economic substance rules and of territorial taxation.

To make sure that offshore companies remain a convenient tool for international business, let us consider the advantages (and, of course, drawbacks) of these companies.

Offshore company pros and cons

What are the offshore company’s advantages?

- quick incorporation of offshore companies (as opposed to the lengthy registration of so-called onshore* companies);

- relatively low cost of both incorporation and subsequent maintenance of an offshore company;

- no obligation to audit or submit financial statements to any authorities;

- no taxes in the country of incorporation (subject to certain conditions for the type and/or geography of business);

- comfortable regulatory environment developed, in particular, to attract foreign investment;

- high level of company ownership confidentiality;

- greater protection of the owners of business from misappropriation of their property.

*onshore companies are companies incorporated in non-offshore jurisdictions (for example, European companies)

Let us take a closer look at some of these advantages.

The incorporation costs of an offshore company are usually significantly lower than those of an onshore company. The same is true of the maintenance costs. There are three main reasons for that:

- the fees of service providers (registered agents), lawyers, accountants, and auditors in “non-offshore” jurisdictions are higher than the fees of their offshore counterparts;

- offshore companies are normally exempt from financial and tax reporting, or auditing financial statements, or paying taxes in the country of incorporation;

- onshore companies often have to rent an office in the country of incorporation and hire local employees (for whom not just a salary, but various contributions such as social security, health insurance, and pension ones must be paid).

It is also worth speaking in more detail about the confidentiality of offshore company ownership. Despite the move towards greater business transparency (meaning transparency of company ownership, complete clarity regarding the activities of companies, transparency of financial flows, etc.), most offshore jurisdictions do not yet have public registers of companies’ beneficial owners. The details of ultimate beneficial owners are, of course, requested, but kept by registered agents internally and/or submitted to government authorities or centralized registers where this information is only accessible to officers of certain departments. Hence, the beneficial owner’s data is not available to the general public.

A complete and unconditional confidentiality no longer exists; it is a thing of the past. We can only say that offshore companies provide a high degree of data protection within the current framework set by international organizations and associations.

When discussing confidentiality and tax benefits offered by offshore companies, it should also be noted that classic offshore jurisdictions do not usually participate in bilateral Double Taxation Agreements (such agreements, among other things, contain provisions on exchange of tax information). It simply does not make sense to make agreements on the avoidance of double taxation with offshore companies: since offshore companies are practically exempt from tax in their countries of incorporation, there is usually no risk of double taxation. However, recently, as part of the same move towards greater transparency, offshore jurisdictions enter into international agreements of a different type – bilateral Agreements on Exchange of Information on Tax Matters (Tax Information Exchange Agreements).

Speaking of international treaties, we cannot but mention the multilateral Council of Europe/OECD Convention on Mutual Administrative Assistance in Tax Matters, which many classic offshore jurisdictions have already joined. The list of countries participating in this Convention is available here.

Offshore company’s drawbacks

You can say that the main drawback of offshore companies is the difficulty they face when opening bank accounts. The banks’ prejudice against companies from offshore jurisdictions most often stems from the fact that these jurisdictions constantly get on the so-called black and grey lists of various international organizations and associations such as OECD*, FATF**, EU***. However, it is precisely to avoid such lists that these jurisdictions implement the legislative reforms mentioned above. Besides, if an offshore company, though not required to do so by law, does prepare financial statements under the International Financial Reporting Standards (IFRS) and does get them audited, say, by a European auditor, then it has a much better chance of opening a corporate account.

*there are currently no countries on the OECD black list – you can see it for yourself here

**FATF black and grey lists can be checked here

***EU list of non-cooperative jurisdictions for tax purposes is available here

Comparative table

The job of understanding advantages and drawbacks of offshore companies and choosing the option best suited for your needs can be made easier with a comparative analysis of the key features of both types of companies:

|

Comparison criteria

|

Offshore Co.

|

Onshore Co.

|

|

Incorporation and maintenance costs

|

lower

|

higher

|

|

List of documents required for company incorporation

|

standard list of documents [see below Stage 2 of the offshore company incorporation procedure]

|

an extended package of documents may be required [may include police clearance certificates, documents confirming the source of wealth / origin of the client’s funds, etc.]

|

|

Company incorporation time

|

shorter [usually from a few days to 2 weeks]

|

longer [usually 3-4 weeks, longer in some jurisdictions]

|

|

Requirement to prepare and submit financial statements

|

no [all offshore jurisdictions have a requirement to maintain and keep accounting records and underlying documentation, but have no requirement to prepare financial statements; some offshore jurisdictions have recently begun to introduce mandatory preparation (so far without filing with any authorities) of simplified financial statements (financial summaries); also, following the introduction of substance rules and/or territorial taxation, certain jurisdictions have made it necessary to submit additional reports/forms]

|

yes [in addition to the requirement to keep accounting records and underlying documentation, onshore companies are often required to prepare and submit to the authorities both financial statements and tax returns; financial statements are prepared under the International Financial Reporting Standards or local accounting standards]

|

|

Requirement to audit financial statements

|

no

|

yes [the requirement to audit financial statements may not apply to all onshore companies – it may be conditioned on the company exceeding certain thresholds in terms of turnover, net assets, and number of employees]

|

|

Taxation in the country of incorporation

|

no

|

yes

|

|

Confidentiality

|

higher [registers of directors, shareholders, and beneficial owners, most often, are non-public, not publicly accessible]

|

lower [in onshore jurisdictions, registers of directors, shareholders, and beneficial owners are often public or the information can be obtained by making a request to the authorities and paying a small fee; plus, if a company is required by law to file financial statements, third parties may get access to them]

|

|

Jurisdiction’s reputation

|

lower

|

higher

|

|

Possibility of opening a bank account

|

limited [opening a bank account for an onshore company is much easier than for an offshore company]

|

much higher [it is often possible to open an account in the company’s country of incorporation, which is an additional advantage]

|

|

Ability to take advantage of bilateral double taxation agreements

|

no

|

yes

|

Some aspects specified in the table have already been discussed, while others deserve to be described in greater detail.

How to choose the right jurisdiction for incorporation of a company?

The choice of a country for company incorporation is always individual: even offshore jurisdictions may significantly differ from one to another in their regulation of certain corporate aspects.

So what affects the choice of jurisdiction for setting up a company?

Various factors must be taken into account:

- activity that the company is going to engage in;

- geography of business;

- whether the client is ready to have a physical office in the country of incorporation (for example, if the jurisdiction has economic substance legislation and the client's activity qualifies as “relevant activity”);

- how much money the owner is willing to spend on the incorporation and subsequent maintenance of the company (this point is closely connected with the previous one – having an office usually significantly increases company administration costs);

- requirements of the main counterparties of the future company and of the bank where the company is going to open a corporate account; and of course

- the needs and preferences of the business owner (owner of the future company).

What is the procedure for incorporating an offshore company?

The offshore company incorporation procedure will certainly depend on the jurisdiction chosen by the client, however, the general course of action will always be as follows:

Stage 1 – it is necessary to decide on important corporate aspects

The business owner needs to choose the name of the future company. Here the client’s wishes must be checked against the laws of the country of incorporation, specifically the rules applicable to company names:

- what words and phrases are prohibited (this can be either concrete words specified in the law, such as “state”, “government”, or simply a requirement that a company name cannot contain offensive words and expressions, be derogatory for the honour and dignity of people, etc.),

- what mandatory “elements” a name should contain (for example, it may be an indication of the legal form or field of activity),

- what language a company name should be in,

- whether an abbreviated version of the legal form is allowed, etc.

Also, in any jurisdiction, the name of a company to be incorporated is necessarily checked for its availability, so it does not coincide with the names of existing companies (more details on this are given in Stage 6 of the company incorporation procedure).

In addition to the name, the client needs to decide on the company structure (director and shareholder), the size of share capital and the distribution of shares (interests) between the shareholders (members). All these elements are country-specific – we will be happy to help you make sense of all this.

Stage 2 – it is necessary to provide documents for the directors, shareholders, beneficial owners, and attorneys

Documents are required for all persons in the structure of the future company. The list of necessary documents will depend on the peculiarities of the jurisdiction and some other factors, but the minimum basic list for an individual includes two major items:

- proof of ID (passport, ID card);

- proof of address (utility bill, bank letter/statement showing the address, etc.).

The minimum basic list of documents for a legal entity (for example, if a company is incorporated with a corporate shareholder) includes:

- Certificate of Incorporation;

- Memorandum and Articles of Association / Charter;

- document confirming the registered office of the company*;

- document(s) confirming the corporate structure*;

- documents leading up to the beneficial owner(s) of the company;

- documents used as proof of ID and proof of address for all individuals in the company structure.

*information both about the address and the structure of the company can be found in a document called the Certificate of Incumbency

In different jurisdictions, the above documents may be called differently and may have a slightly different meaning or perform a different role, that is why we recommend that you seek specialist advice and request a finalized list of required documents.

Stage 3 – it is necessary to undergo a compliance check

Nowadays, no one is surprised by the requirement to undergo a mandatory compliance check. Everyone knows that compliance is an internal control system aimed at identifying violations of the requirements of the legislation in a particular jurisdiction (for example, if you want to register a Seychelles company, the company’s activities and other aspects will be checked for their compliance with Seychelles laws).

A compliance check is also meant to identify potential risks for the registered agent that will establish and then administer the client’s company. In most countries, registered agents obtain licences to conduct their business. Licensed activities are known to always be subject to stricter scrutiny, with regulators conducting periodic inspections of the regulated organizations. If the regulator discovers numerous violations of the law by the clients of a registered agent or by the agent itself (for example, regarding the keeping of statutory company documents and information about the client), or if there is a major scandal related to the administration of clients charged, say, with money laundering, then the registered agent will face extremely unpleasant consequences:

1) significant fines; and/or

2) revocation of the licence to do business.

We are not even mentioning the reputational damage such scandals cause to a registered agent (it can still lose clients whilst keeping the licence). It is easy to figure out that registered agents will not put their entire business at risk because of one or a few clients, so be ready to provide certain requested information and, in some cases, supporting documents. This is common practice nowadays and not something out of the ordinary.

To run the initial compliance check, the registered agent usually requests information about the proposed activities of the company, the countries where it expects to operate, and the details of individuals in the company structure (see Stage 2 of the company incorporation procedure above). After receiving this information, a check is done within the framework of the so-called KYC procedures. KYC is an abbreviation for “Know Your Client” (or “Know Your Customer”). Effectively, this is a client identification procedure.

Stage 4 – it is necessary to pay for company incorporation and accompanying services

The cost of incorporating an offshore company usually includes the following services:

- preparation of documents required for company incorporation;

- payment of the government fee for company incorporation;

- payment of the local registered agent’s fees for the first year of company administration, including the provision of a registered office address;

- preparation for the client of a set of company documents and the seal (if having a seal in a particular jurisdiction is either mandatory or desirable).

A compliance check is a separate cost. Accompanying services that may potentially be needed include additional advice on various matters, creating economic substance in the country of incorporation, obtaining tax/legal opinions from local specialists, translations, etc. These are just examples. Whether any accompanying services are needed and, if so, their exact list will all depend on the jurisdiction in which the company is incorporated, the activity that the client is going to conduct, and other factors.

Stage 5 – it is necessary to prepare a package of documents for company incorporation

This stage is about preparing a package of documents to be signed by directors, shareholders, and beneficial owners and sent to the company’s country of incorporation. If possible, documents are prepared in parallel with actions described in the next Stage (to speed up the incorporation).

Stage 6 – it is necessary to apply for company incorporation

As mentioned in Stage 1 and even before that, the client needs to decide on the company’s name, as well as the jurisdiction. If the chosen jurisdiction allows checking a company name for availability in advance and reserving it, then by Stage 6 of the incorporation, the name is already reserved. Therefore, we apply to the registrar for the incorporation of a company with the specified name. If it is not possible to check the availability of the name in advance and reserve it, then there is a chance the application may be rejected because the name coincides with the name of an existing company; in this case, the application will need to be re-submitted with a different name. However, the name check option is usually available in one format or another, so such rejections are rare.

Then the registrar establishes a company and assigns it a state registration number (in offshore jurisdictions, it is often called a company number).

Stage 7 – it is necessary to complete company incorporation

We have now reached the final stage of a new company setup process.

This stage sees the finalization of corporate documents, with the approved company name (if it was not approved and reserved before the incorporation) and the state registration number assigned to the company.

One set of documents is sent to the country of incorporation* if these documents were not sent at Stage 5 or were not sent all, while the other set** is delivered to the client.

* these are normally the documents that must be kept in the local registered agent’s files (for example, director’s consent to his appointment, resolution/declaration stating the address for keeping accounting records and underlying documentation of the company, KYC documents)

** the client receives the Certificate of Incorporation, Memorandum and Articles of Association, resolutions on the election/appointment of directors, shares certificates and other documents depending on the country of incorporation of the company

What is the incorporation time for an offshore company?

The following factors will influence the incorporation time frame of an offshore company (and not only an offshore one):

- jurisdiction in which the company will be incorporated (as government agencies in different jurisdictions process applications at a different speed);

- how the procedure is organized – directly or through a chain of intermediaries (the more intermediaries are in the chain, the longer all procedures take, not just incorporation);

- corporate structure of the future company (if all persons in the company structure are individuals, incorporation is usually completed quicker; if the director or, more often, a shareholder of the company is a legal entity, incorporation takes longer);

- how quickly the client provides the documents and information required to complete all stages of the company’s incorporation, including compliance checks;

- whether the provided documents need to be translated into the official language of the jurisdiction chosen by the client (it is not always English), etc.

In most of the popular offshore jurisdictions, most of the time it takes 2 – 3 business days from the completion of preparatory stages and filing of the application for incorporating a company to the assignment of a state registration number to it. In jurisdictions where we ourselves are licensed as registered agent, we usually manage to obtain company registration confirmation within 1 business day. It will then take some time to prepare the final set of documents, get them apostilled (where applicable) and delivered to the client – usually a week or two. From our end, we make every effort to ensure that all the stages of incorporation are completed as quickly as possible.

Can the company’s jurisdiction be changed after incorporation?

It may happen that the jurisdiction that the client chose to incorporate and operate a company in, introduces changes in its legislation which will start adversely affect the use of the company. Or the client’s business may undergo significant changes which will necessitate the change of the company’s jurisdiction. For these cases, there is a special procedure called redomiciliation (another term used is continuation).

In most jurisdictions, the redomiciliation of a company, i.e. its “relocation” from one jurisdiction to another, is allowed both “in” and “out”. This means that if a country permits redomiciliation, then it usually allows companies to be redomiciled both to its territory and, vice versa, outside its territory. However, there may be exceptions to this rule or special conditions or limitations. For more detailed information on the jurisdictions you are interested in, please contact the consultants of our company.

Transferring a company from one jurisdiction to another is usually much more expensive than incorporating a new company in another jurisdiction. However, redomiciliation is still very popular because it allows changing the company’s country of incorporation, while retaining all existing business relationships (and often also the company name and even the bank account).

Can the name of an already incorporated company be changed?

Of course, it can. The new name will also be checked for availability and compliance with the rules of the company’s country of incorporation.

Changing the company name will involve additional steps and costs. These include:

• preparing documents required to change the name;

• paying the government fee for filing the name change;

• making changes to the corporate documents and registers;

• submitting additional notifications to the authorities or centralized databases (will depend on the jurisdiction).

What does the subsequent maintenance of an offshore company include?

Renewal

Offshore companies must be renewed annually to remain on the register of companies. As a rule, the renewal includes the payment of/for:

• government fee,

• registered office address and other services provided by the registered agent (for example, submission of the Annual Return or other reports and forms),

• services of professional directors/shareholders (if appointed in the company),

• compliance check.

Depending on the jurisdiction, annual filing of various forms may be required. For example, many countries, together with payment of the government fee, require submitting to the registrar a report called the Annual Return. This report is necessary to confirm the current structure of the company, the size of its authorized capital and any other details.

In addition, as mentioned earlier, some jurisdictions, following the introduction of economic substance legislation, may require to annually submit forms confirming that the company does not conduct the “relevant activity” specified in the law (if it does not indeed). Such forms are usually submitted during the renewal of the company too (together with payment of the government fee).

And one should not forget that companies in any jurisdiction must periodically update the information for compliance purposes.

Maintaining and keeping accounting records

Companies incorporated in any offshore jurisdiction are required to maintain accounting records and keep them together with the underlying documentation related to the company’s business activities. Various countries may phrase the rule a little differently, but this requirement is ever-present.

A company usually can choose where to keep such records and documents:

• at the registered agent’s address (which is usually the same as the registered office of the company)*; or

• at any other physical address.

*this service is usually provided by registered agents for an additional fee

If a company chooses to keep documents not at its registered office, it must notify its registered agent of the address where the original accounting records and underlying documents are kept.

Accounting records and underlying documents must:

- be reliable and objective;

- be sufficient to reflect and correctly explain the company’s operations;

- enable at any time the company’s financial position to be determined with reasonable accuracy;

- enable the preparation of the company’s financial statements (if required).

These rules do not imply mandatory preparation of financial statements under local accounting standards or IFRS; such a requirement has not yet been introduced for offshore companies. But bear in mind that some jurisdictions already require offshore companies to prepare financial statements in a simplified form (the so-called financial summary).

Can an account be opened for an offshore company?

Yes, it is possible to open an account for an offshore company, although this is not the easiest of tasks. In all fairness, nowadays it is not that easy to open an account for any company. Banks and payment systems are bound by a lot of rules and regulations, both national and international. In addition, each financial institution also has its own internal regulations and client policies (regarding jurisdictions of companies, types of their activities, necessary turnover, account balances, and much more). Some banks are traditionally classified as savings or investment banks (these are banks that are aimed at preserving accumulated assets, such as most Swiss banks), while others are settlement banks (these are banks that are ready to work with companies which actively do business and make a large number of transactions).

Is automatic exchange of information relevant to offshore companies?

The short answer is: yes, it is. However, this is not connected with companies themselves, but with their accounts opened at banks and payment systems.

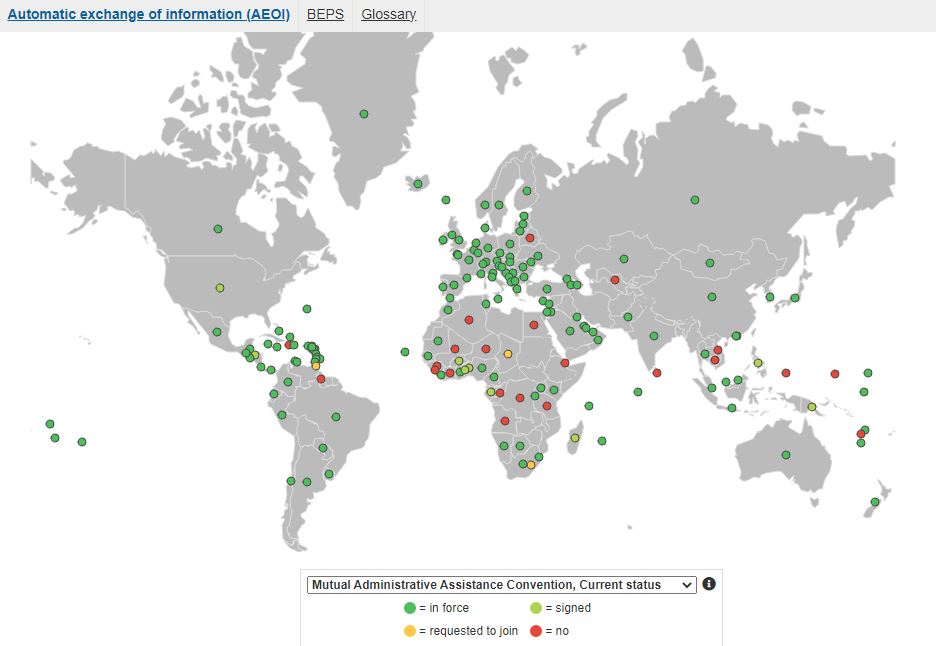

We mentioned above the Mutual Administrative Assistance Convention, also saying that a lot of countries are parties to it. Automatic exchange is carried out on the basis of this particular Convention, as well as the Standard for Automatic Exchange of Financial Account Information in Tax Matters (Common Reporting Standard, or CRS). How countries are covered by automatic exchange of information is shown on this map from the OECD website.

The information so exchanged is received not from registered agents administering companies, but from financial institutions in which companies hold their accounts. Therefore, when we talk about automatic exchange, what matters is not whether the country of the company’s incorporation is a party to the Convention, but whether the country of the company's bank account is a party to it and whether the jurisdiction has started exchanging information yet.

A heads-up: the overwhelming majority of jurisdictions that are home to “reputable” banks (which are considered reliable and trustworthy) are parties not only to the Convention, but also to all additional documents formalizing the operation of the automatic exchange of information on financial accounts.

Many countries introduced automatic exchange on 1 January 2018, and in July 2019, 90 countries exchanged information on 47 million accounts with a total value of EUR 4.9 trillion. Also, according to the OECD, voluntary exchange of information in the run-up to the implementation of the above-mentioned standard brought EUR 95 billion in additional tax revenue for OECD and G20 countries.

So automatic exchange of information works and quite successfully. Of course, there are nuances here as well. You can seek advice on this subject from our specialists who will answer all questions and analyze your case.